Highlights

The Earned Income Tax Credit (EITC), which provides a tax credit of $2,982 on average to low-income working parents when they file their taxes each year, is among the nation’s most vital anti-poverty policies. In its current form, the credit becomes more generous to very low earners as they work more. At a certain level of household income, however, the benefits are phased out—and this set-up comes with a number of drawbacks.

For example, a single mother with a modest annual income and one qualifying child could obtain as much as $3,305 from the federal EITC. If she marries an employed man, their credit would shrink as the EITC is phased out. This is one example of a means-tested program that can dissuade working mothers from marrying the father of their newly-born child and incentivize them to simply cohabit instead.

A second problem with the current EITC and the tax system more broadly is that they provide virtually no benefits to lower middle-class parents. Such families have too much income to qualify for the EITC, but not have enough income to avail themselves of several child-related programs benefiting those in the upper-half of the income distribution—flexible spending accounts, childcare tax credits, and pretax college-savings plans. In a widely circulated 2000 paper, David Ellwood and Jeffrey Liebman labeled this the “middle-class parent penalty.”

To address both problems, I have put forward the New Mothers’ Tax Relief proposal, which constructs an alternative EITC schedule for families that have one qualifying child under the age of six. It provides a more generous EITC for these families by raising the income level at which the phasing-out of credits begins—to $42,000 for married couple and $19,000 for head-of-household families—and lowering the phase-out rates to 6 percent for married couples and 12 percent for head-of-household families.

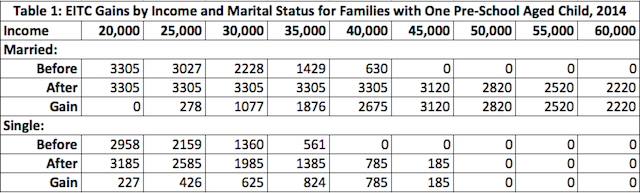

Table 1 indicates the additional income these changes would provide to families depending on their marital status and incomes: more than $2,000 to married couples with incomes between $40,000 and $60,000 and at least $600 to head-of-household families with incomes between $30,000 and $40,000. (These exact same benefits would be grafted onto the EITC schedules for those households that have additional children in the family.) All of the benefits are targeted to families with young children, who are the families that most need the extra credits to pay for their added expenses.

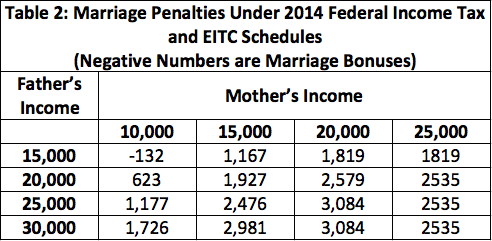

My proposal also ensures that the tax system will not penalize couples for marrying. Many child advocates are concerned that more and more children are being raised by unmarried parents, and one factor behind the drop in marriage rates may be safety net programs that are more generous to single parents. Table 2 indicates the size of the current federal marriage penalty—the amount of money a couple stands to lose if they marry—as we vary the incomes of the two partners. If a single mother with one child earns $15,000, she would receive the maximum EITC, but if she marries a partner earning $25,000 the EITC they receive would drop to $630, a reduction of $2,675. While they will save a bit on other federal income tax liabilities, their disposable income will be lowered by $2,476. In some cases the marriage penalty reaches $3,000, or far more if the single mother qualifies for state EITC programs and other means-tested safety net programs.

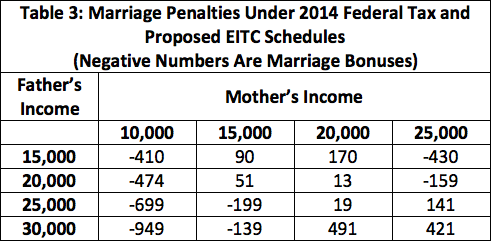

By increasing the income level for married-couple families at which the phase-out of EITC benefits begins, we can eliminate the federal marriage penalty for a wide range of working partners, and in some cases actually provide marriage bonuses (Table 3). For example, the hypothetical couple I described above would gain a marriage bonus of $199 rather than pay a marriage penalty of $2,476. These changes will allow many new parents to base a marriage decision on factors other than the federal marriage penalty they currently face. In addition, the additional funds for lower-earning married couples will reduce their financial stresses, which can exacerbate relationship tensions that sometimes lead to divorce.

The New Mothers’ Tax Relief proposal is well targeted. It only provides benefits to families with pre-school aged children. While all married couples with incomes up to $97,000 will gain some benefits, the vast majority of the benefits go to families with income less than $60,000. As a result, it is likely that the proposal will cost around $16 billion annually if extended to children under age six, or less than $10 billion if limited to families with a child under three.

There are other proposals aimed at reducing the federal marriage penalty that working single mothers face, but they are much more expensive and often require a number of changes to the tax system. By contrast, this proposal doesn’t increase the complexity of filing taxes. Families will simply choose which EITC schedule to use: the current one or the new one depending on whether they have a qualifying young child. It is about time that we target benefits to families with very young children, and by doing it through the EITC, we can largely eliminate the federal marriage penalty low-income mothers face at the same time.

Robert Cherry is Stern Professor in Economics at Brooklyn College and the Graduate Center of the City University of New York.